🔔Week Overview: New Month New Market

& China Tariffs

I hope everyone is having a wonderful labor day and extended time away from the work week! With a short week in the markets and not that much data, it will most likely be a pretty quiet and less volatile week.

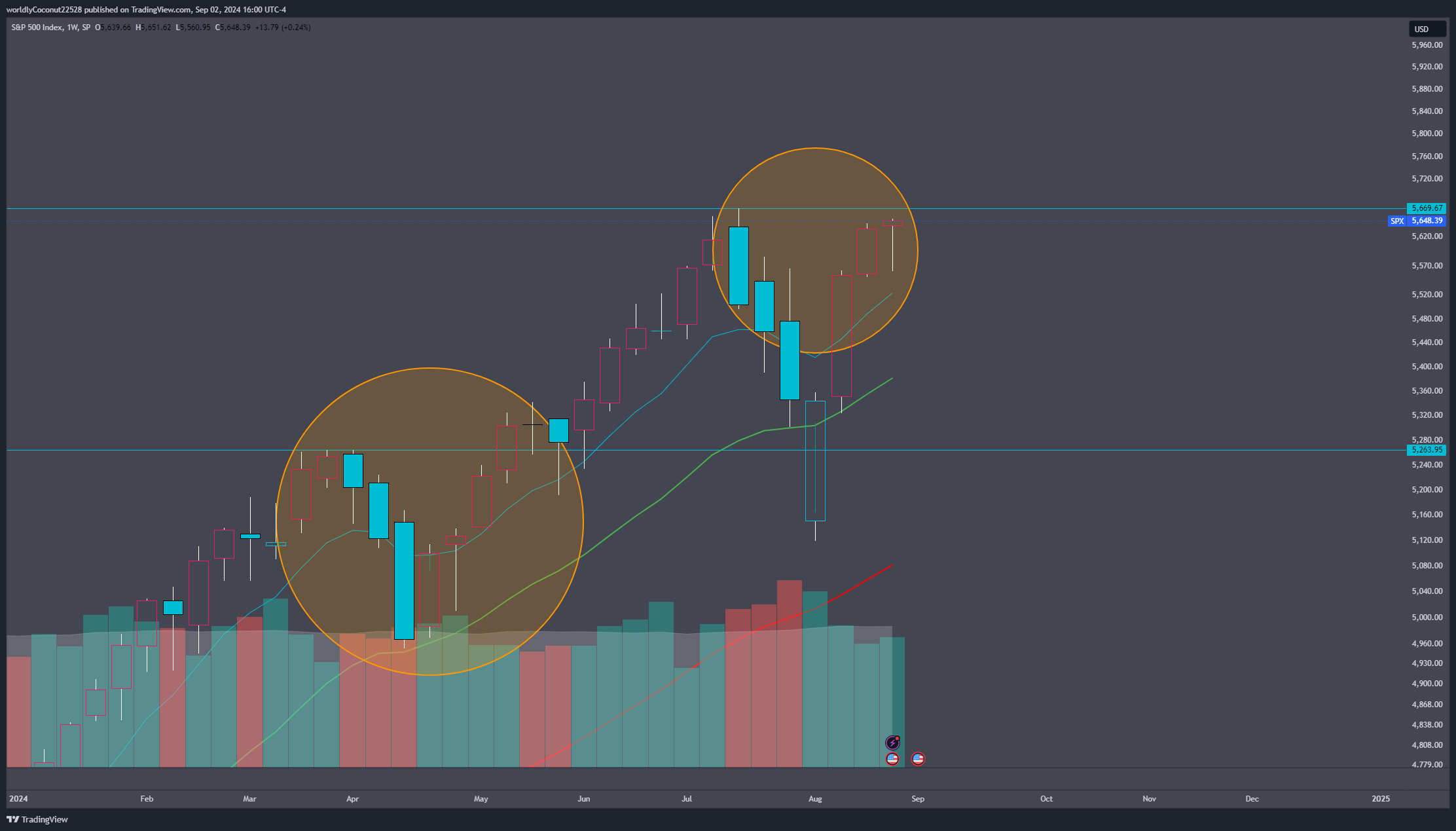

We enter September with SPY 0.00%↑ about only 0.25% away from ATHs. Some traders are viewing this as new ATHs are going to made with a lot more steam left in this rally. We saw quite a run the last time we saw a potential double top in the market earlier this year.

This is puts us in a very interesting spot for the new month because September tends to be a more negative return period of time. I still stand firm in my thesis that we get a run up into September FOMC on 9/17 and then potentially pull back as a sell the news to close out the month!

Notable Data:

Thursday

ADP Non-Farm Employment Change 8:15 AM

ISM Services PMI 10 AM

Friday

Unemployment Rate 8:30 AM

Notable Earnings:

Tuesday

Wednesday

HPE 0.00%↑ , DLTR 0.00%↑, DKS 0.00%↑

Thursday

AVGO 0.00%↑, DOCU 0.00%↑, NIO 0.00%↑

Friday

Only time will tell if DG 0.00%↑’s horrible earnings report was an early red flag of rougher economic times to come or if it’s just a company not being run properly. DLTR 0.00%↑’s earnings report should give us more insight into this. The other notable earnings this week is AVGO 0.00%↑, which should give us more chip stock momentum.

📊Data Boost

The positive looking data that came in last week was a large contributor to the strong close on August.

Consumer confidence on 8/27 reported 103.3 vs 100.9 expected.

GDP on 8/29 came in at 3.0% vs 2.8% expected, Unemployment claims came in slightly lower at 231k vs 232k expected. And Core PCE came inline at 0.2%.

These numbers tell us that consumers are confident in their current and future financial conditions, which can be supported by the lower unemployment claims. This goes hand in hand with higher GDP, which points at an increase in economic activity.

What I find conflicting is that DG 0.00%↑’s most recent quarterly report saw the majority of their customers feeling more financially squeezed these past few months. The majority of Dollar General’s customers make less than $35,000 a year. Could it be that the middle class is beginning to stabilize and it will take some more time before the lower wage group of people see financial easing?

📦China Tariffs

As we approach election time, it’s interesting to observe how some companies are reacting to who might be elected. In 2018, President Trump introduced a tariff on Chinese products in an effort to strengthen US production. President Biden continued this tariff and even extended it to products like solar cells and EVs.

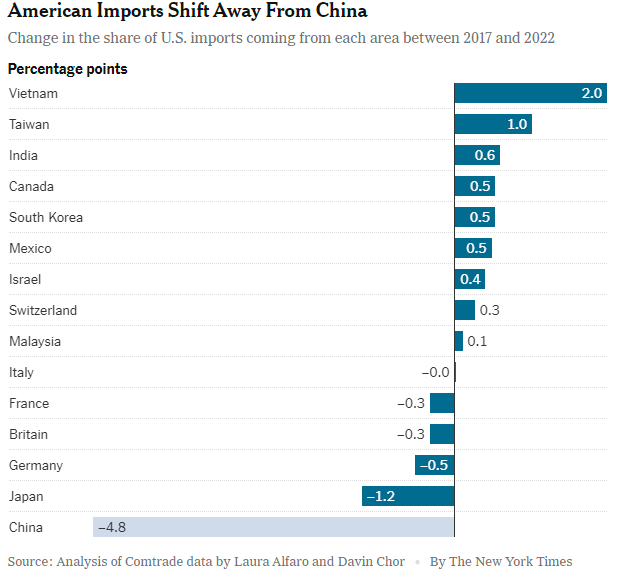

Running again, Trump has proposed an additional tariff of up to 60% on all Chinese products, and 10% to all other imports. These costs could significantly impact manufacturers and and retailers. Regardless of which party is in power, it’s likely that tariffs on China products will continue and potentially be higher. This can shift imports to other countries like India. A survey of American companies with Chinese imports in 2023 actually reported over 40% of the companies are planning pivots to other countries because of rising tensions.

Was pivoting to other countries the intention?

The tariffs were originally introduced to encourage more American manufacturing. Instead, it seems like companies are maneuvering to other low wage countries like Vietnam, India, and Mexico.

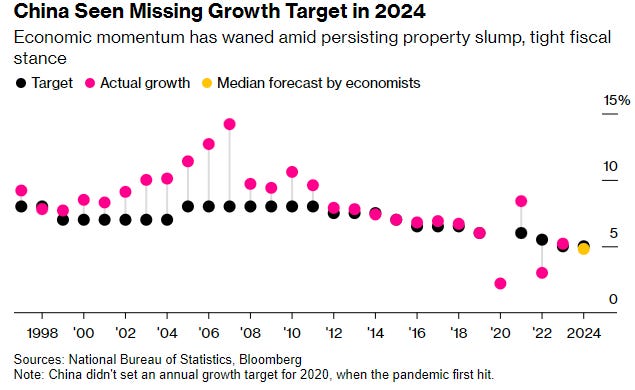

The above data ends at 2022, but it’s clear that the pivot away from China manufacturing is in full effect. Europe raised tariffs on imported Chinese EVs up to 36% in June 2024 and the economic effect can already be felt. China factory activity declined for a fourth straight month in August, signaling stalling economy activity for the country.

With China housing issues on the rise as well, the global economies will be watching closely on what further action China takes in response to waning economic growth. China saw new home sale values decline over 26% compared to last year. As a response, the Chinese government is allowing home owners refinance up to $5.6 trillion dollars worth of mortgages in an effort to boost consumption. Of course, this will negatively impact the profitability of state-run banks and potentially help transfer some wealth to China’s people. Economists also anticipate banks in China to cut mortgage rates even more as an effort to help boost more economic activity going into the rest of the year. We will probably see more urgency from the Chinese government the closer we get to the end of the year.