🔔Week Overview: Jackson Hole & Recession Risk

+ Thoughts on NKE and SBUX

Happy Sunday!

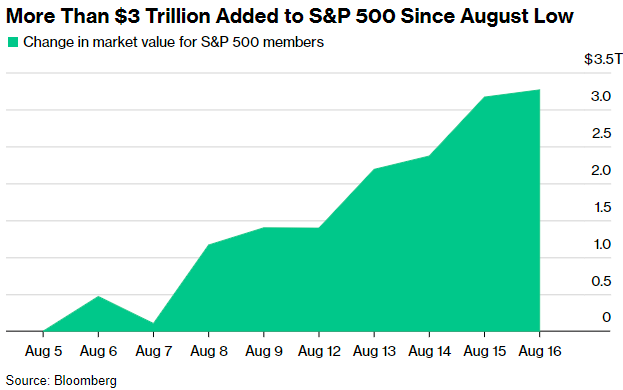

TLDR: We had an overreaction to recession fears while the Bank of Japan raised interest rates furthering the selloff in the US stock market. The largest catalyst we have this week is Powell’s speech on Friday at the Jackson Hole Economic Policy Symposium. All eyes are set in preparation for September’s FOMC and the expected interest rate cut.

As we wrap up August, let’s recap what has happened recently. Early August, we saw a weaker than expected July jobs report while unemployment rose to 4.3% (highest since 2021). This sparked recession fears into stock market participants leading to a selloff globally. It also didn’t help that the Bank of Japan (BoJ) raised interest rates in Japan causing even more of a sell off.

Why would interest rate hikes in Japan cause a selloff?

Investors around the world were utilizing a form of arbitrage called carry trades, where you borrow in a currency that has a lower interest rate like the Japanese Yen to reinvest into other more risk-on assets. Carry trades made sense with the Japanese Yen since interest rates in Japan were negative/0% until recently as rates are now 0.25%. Because the return was less favorable, investors were forced to either cover or start to sell their position in their higher yielding assets. In my opinion: This was unfortunate timing in the sense that the US stock market got a recession scare with the weak job report and then investors that were over leveraged through the Japanese Yen had to rebalance their risk.

In uncertainty and fear, I am always reminded of Warren Buffet’s investing thesis:

“We sell really when we think we're reevaluating the economic characteristics of the business.”

i.e. The stock price is not always indicative of the business’s performance. This idea also means you shouldn’t sell a stock unless something has fundamentally changed for the business. More on this later when I discuss NKE 0.00%↑ and SBUX 0.00%↑.

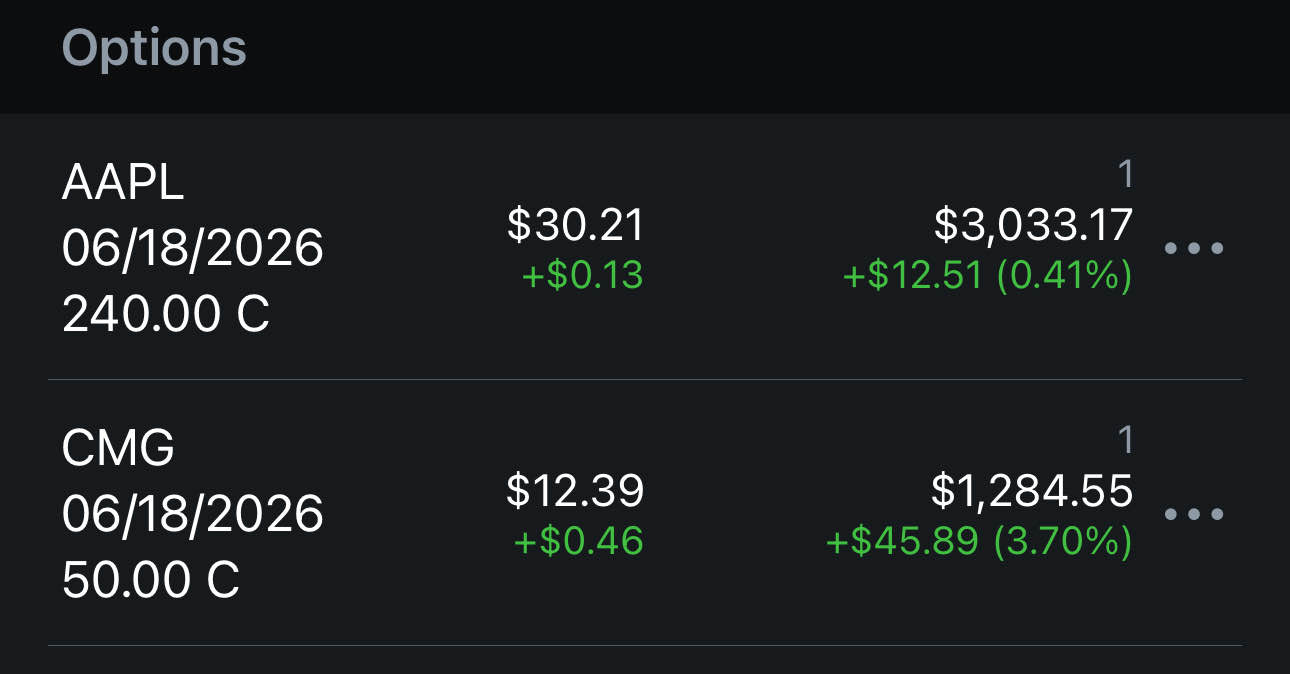

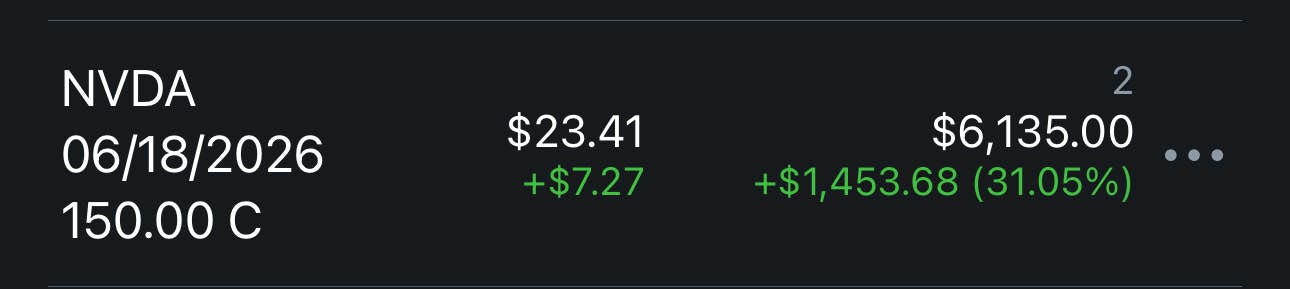

I put my money where my mouth is, I truly viewed what happened in the stock market as an overreaction. Aside from DCA’ing into VOO 0.00%↑ and QQQ 0.00%↑, I also purchased leap contracts into AAPL 0.00%↑ , CMG 0.00%↑ and NVDA 0.00%↑.

I chose a mix of either ITM or close OTM strikes because these are on my long term portfolio. I would rather treat them as buying 100 shares over trying to maximize the delta on these contracts with more OTM strikes. I will update these as we go into the 2025.

👉Catalysts This Week

Monday, August 19: FOMC Waller speaks 9:15AM

Tuesday, August 20: FOMC Bostic 1:30PM & Barr 2:45PM

Wednesday, August 21: FOMC Meeting Minutes 2PM

Thursday, August 22: Unemployment Claims & PMI 8:30AM

Friday, August 23: Powell speaks at Jackson Hole 10AM

The market is currently already pricing in rate cuts to begin in September, with probabilities up to basically 100%. Because the stock market can tend to be very anxious, participants are looking for some form of confirmation of rate cuts from Powell at the Jackson Hole Economic Symposium this Friday.

Confidence of rate cuts in September signals an almost guarantee of it happening. Investors are now looking to see how big of a cut as well as Powell sounding more dovish than hawkish during his Jackson Hole speech. This is because the market is looking for reassurance from Powell that the soft landing they had in mind is coming into play. The weak July jobs report contradicts what the Fed is attempting, which is why we had the recession fear.

Nike & Starbucks Woes

We saw NKE 0.00%↑ suffer a -18% decline post earnings earlier this summer after reporting a -2% in revenue YoY. At the lowest, the stock was down almost -25% from pre-earnings prices. This can be attributed to a lack of direction and waning brand dominance in the industry as brands like Hoka and OnCloud have become popular. This inflection point is clear as day because while Nike guided down for the rest of the fiscal year, Adidas actually raised their full year guidance in their most recent earnings report.

Funny enough, the stock is now up over +18% as Pershing Square Capital Management LP (Bill Ackman) disclosed a long position in the company.

More importantly (in my opinion), Nike has rehired Tom Peddie as vice president of marketplace partners (which focuses on the company’s wholesale sector). It’s interesting because while Nike’s DTC’s revenue stream saw a decline of over 8%, they saw their wholesale sector grow 5% in the quarter. To me, this says that the company recognizes that their current business operations are obviously not working. They recognize that they are seeing strength in their wholesale sector and want someone experienced in that division to steer the ship going forward. Only time will tell if Nike is able to get back on track of if this is truly an inflection point of their brand dominance in the space.

SBUX 0.00%↑ is also experiencing an inflection point in their business, with their most recent earnings report posting another -1% decline in revenue. Same store sales saw a 3% decline and traffic in US stores experienced a 6% drop. In Q2, the company had stated that they wanted to focus more on revitalizing the traffic in US locations. Q3 results show that they haven’t quite figured out the formula for resolving lagging US revenue. The company also made an executive position shift, by appointing Brian Niccol as their new CEO. Niccol is more prominently known for his CEO position at CMG 0.00%↑ in 2018, where he introduced the Chipotlane and optimized the company’s business operations.

I discuss Chipotle’s success here:

From this news, Starbucks stock price saw almost a +25% boost.

While I do believe the poaching (I use this word begrudgingly as an investor in Chipotle) of Brian Niccol indicates Starbucks wants to get back on track, the numbers and results will dictate whether or not the company will get back on top. The changing of CEO does not magically reverse Starbucks’s decline in revenue and traffic, but it does make the future more auspicious. I will be watching closely to see if Niccol’s experience with optimizing Chipotle’s operations can translate well to Starbucks’s business.

Both Nike and Starbucks realize that what they’re currently doing is not working and are actively searching for the right solution. Instead of ignoring issues within the business, both brands are attempting to adapt. This is a better reaction than many other companies who have faced similar challenges. I am not saying Nike and Starbucks are good shorts, but I certainly would prefer to stay sidelined to watch how these two companies navigate their inflection points in their respective businesses.