🏠Renting is the new owning?

🔒Housing market gridlock🔒

Introduction

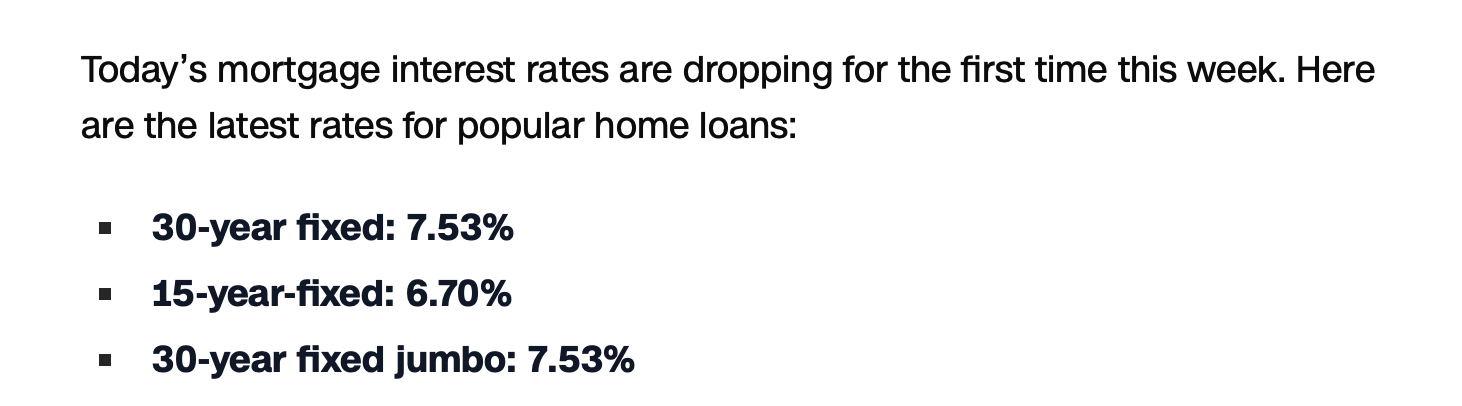

I think what’s currently happening in the U.S. housing market is very intriguing. Current 30 yr mortgage rate as of 5/7/2024 is sitting at 7.53%, with the other rates seen below:

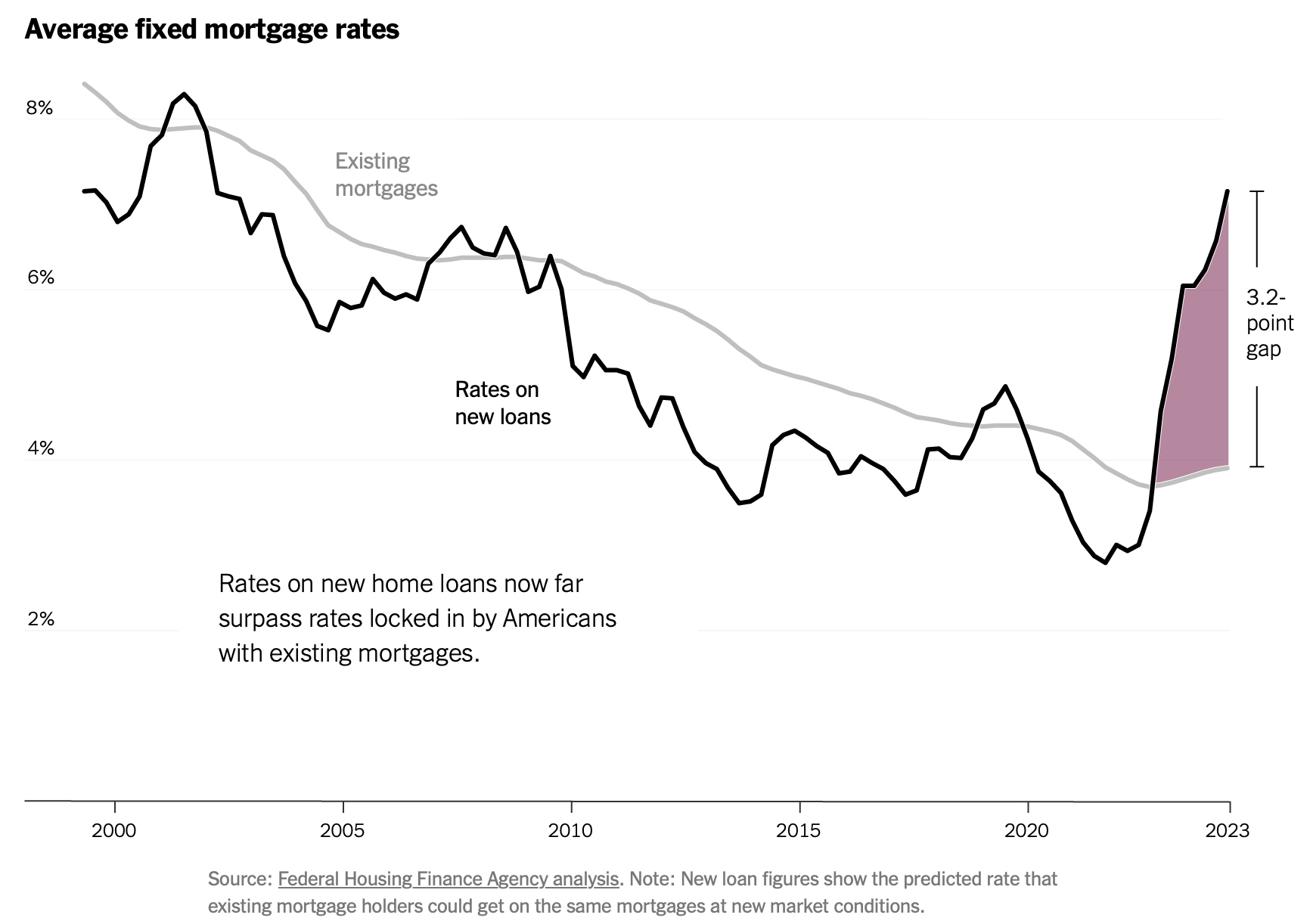

With the rates surpassing what we saw during the 2008 recession, there’s an even more interesting thing happening. Despite high rates, the majority of home owners actually have a mortgage rate ~3.2 % lower than the current market mortgage rate.

In this edition, let’s talk about:

What’s happening in the housing gridlock

What happened during the pandemic & realtors

Housing Gridlock

There are two significant factors in play, on the supply and demand side of the housing market. They crash into each other to reach where we are currently with the housing market.

Supply side:

The majority of current home owners have no incentive to sell their home because they would have to get a new mortgage with a higher rate than the one they currently have. The interest they’d pay on the new mortgage offsets most if not all the appreciation of their current home. So, home owners that might usually relocate for higher pay or downsize are unable to do that. With less supply, current houses on sale are not only still inflated from pandemic appreciation but also from the lack of new supply in the market.

Demand side:

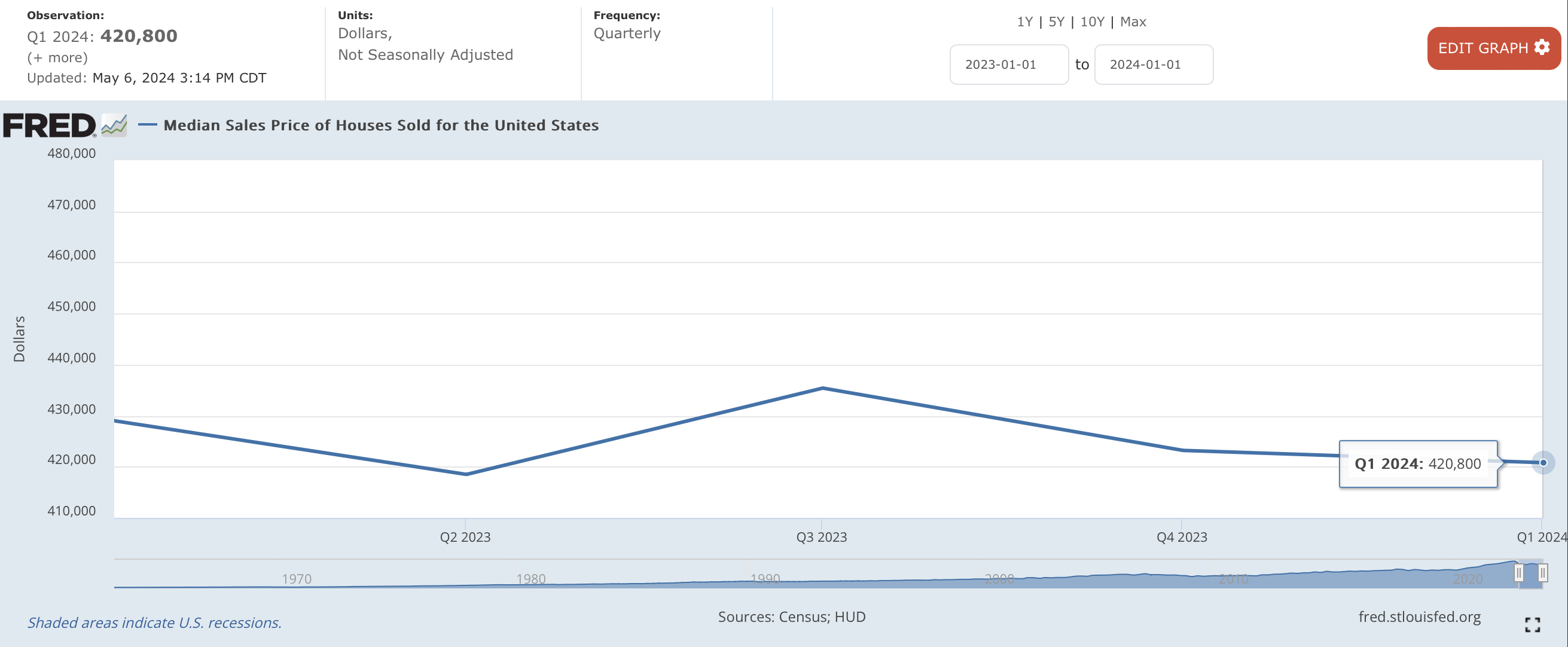

The flip side is that first time home owners are way less inclined to close on a house with higher home prices and higher mortgage rates. At that point, it’s more financially sound to continue renting rather than owning a home. The median sales price of a home in Q1 2024 is $420,800.

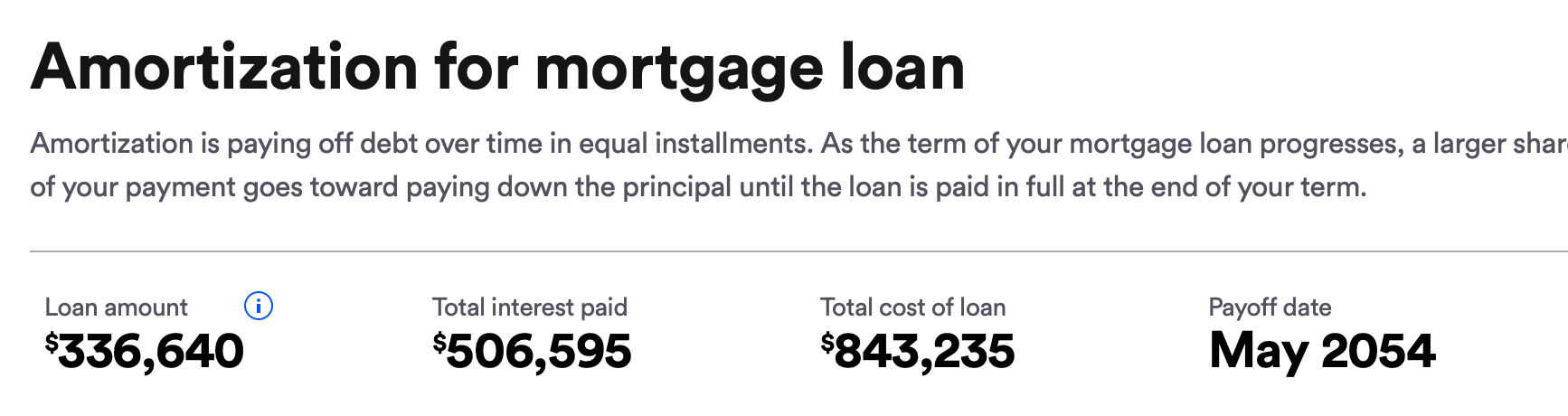

Let’s assume you pay 20% down, with the national average HOA fees of $191, $277 property tax per month, and home owner insurance of $100. Your total interest paid if you go the 30 years is over half a million dollars. That’s ridiculous!

Now of course, you can always refinance or relocate and sell your home. Here’s why that’s not happening:

The Fed has emphasized that they are not planning to lower rates for a while longer. This means home owners will not be able to refinance for a lower rate for the near future. Uncertainty will dissuade potential buyers from pulling the trigger on buying a home.

Home owners would not be able to relocate because they would wind up with the same high mortgage rate. So, renting at that point would be much more economical.

→ How the Fed rate effects mortgage rates

While not directly effecting mortgage rates, the federal funds rate indirectly influences the mortgage rate. Increasing the Fed rate leads to higher costs of borrowing from bank to bank. Higher borrowing costs on a bank level means they will less incentivized in approving loans and/or increase costs on the consumer side. The mortgage rate usually aligns with the 10 yr-treasury note. When the Fed rate goes up, increase in yields will occur, which increase the mortgage rate. This is because government bonds will get sold when the Fed rate increases, which will cause yields to increase to try to get more buyers.

Eventually, one side will have to crack and compensate the counterpart. We’re already starting to see some of this effect happening with housing prices slightly decreasing. We’re starting to see some price cuts, but the strange part is that homes are still getting bought up typically in 17 days. The strength in our labor market and how operational the economy is in these high inflationary times is why the Fed has not reduced the federal funds rate yet.

→ Renting is cheaper

As of April 1, 2024, renting was cheaper in all 50 of the largest US metro areas. And, the monthly cost of buying a home was 60% higher than the cost of renting. With less inventory, higher prices, higher loan rates, it makes way more economical sense to be renting. Not everyone will be in the right situation where not having their own place (usually larger space too), which could be the explanation for why homes are getting bought up pretty quickly still.

Pandemic Housing Market & Realtors

If you haven’t been in the market for a home, I’m sure you saw the craze with realtors in the news. Everyone’s mother was switching careers and becoming a realtor. This is because during the pandemic, mortgage rates were under 3% for the first time ever and houses were selling like hotcakes. With stimulus checks as cash injections to boost the economy with lockdowns, people had way more disposable income. This fiscal policy did help spur the economy, and maybe a little too much.

→ What caused the housing price spikes during the pandemic?

Because of social distancing and lockdowns, people looked for homes that weren’t in urban areas. You didn't have to go into the office anymore. This drove up demand and prices for houses in smaller markets. Once these smaller market homes got bought up and experienced price spikes, people began looking in more urban areas. As typical with demand, all markets now saw price surges.

I remember reading headlines that talked about how home buyers were getting beaten out by six other offers. And all offers would be above asking price. Moreover, realtors began to close deals before they could even start open houses. You have to remember that realtors get paid a commission on each home they sell, which is around 5% to 6% of the closing price of a home. At the average Q1 2024 home price of $420,800, the commission is over $25,000.

It’s in their best interest to sell more expensive homes. There is a clear grey area here where the middle party prefers more expensive homes because they are compensated better. With people responding to the pandemic, and realtors taking advantage of the pandemic economic opportunity, it makes total sense that housing prices sky rocketed across the U.S..

However, in today’s world of high inflation and high mortgage rates, realtors are beginning to struggle. Realtors are having to actually conduct open houses now on their inventory. It also doesn’t help that the National Association of Realtors (NAR) reached a settlement with home sellers to get rid of the 6% commission rate. While not explicitly stating the removal of the 6% commission rate, sellers now have the ability to negotiate the rate. The settlement allows home sellers to not share the commission with the buyer’s agent. Maybe the commission costs were baked into the selling prices. If true, this could lead to potential drops in housing prices.

→ Why is this important?

If we didn’t get the surge post-pandemic in the housing market, we may not have seen the settlement reached with the NAR. The settlement creates a more transparent and fair process for completing the sale of a home. It gives the home seller more negotiating power and could potentially drive down housing prices.

It also shows you how influential the Federal Reserve is when it comes to effecting the economy. We were directly effected by the government when everyone received stimulus checks, which spurred economic activity. And then while not directly effecting you and I when increasing the Fed rate, we feel the trickle down effects. Higher Fed rates have led to a surge in mortgage rates and higher costs for everything else as well. Now, a lot of people are blocked from entering the housing market.