NVDA Beats, Seasonality Effect Incoming?

& Dollar General Warning

What a turbulent week we’ve had so far!

SMCI 0.00%↑ stock has fallen over 25% this week from news that Hindenburg Research has opened a short position on the company claiming Super Micro has been cooking their books. The very next day, SMCI announces that they are delaying the release of their 10-K. Not a good look!

With PCE data coming in tomorrow morning, I believe all eyes on will be focused on the upcoming September FOMC meeting. Honestly, aside from intra day volatility, I don’t think we will see any large moves until the rate cut on September 17.

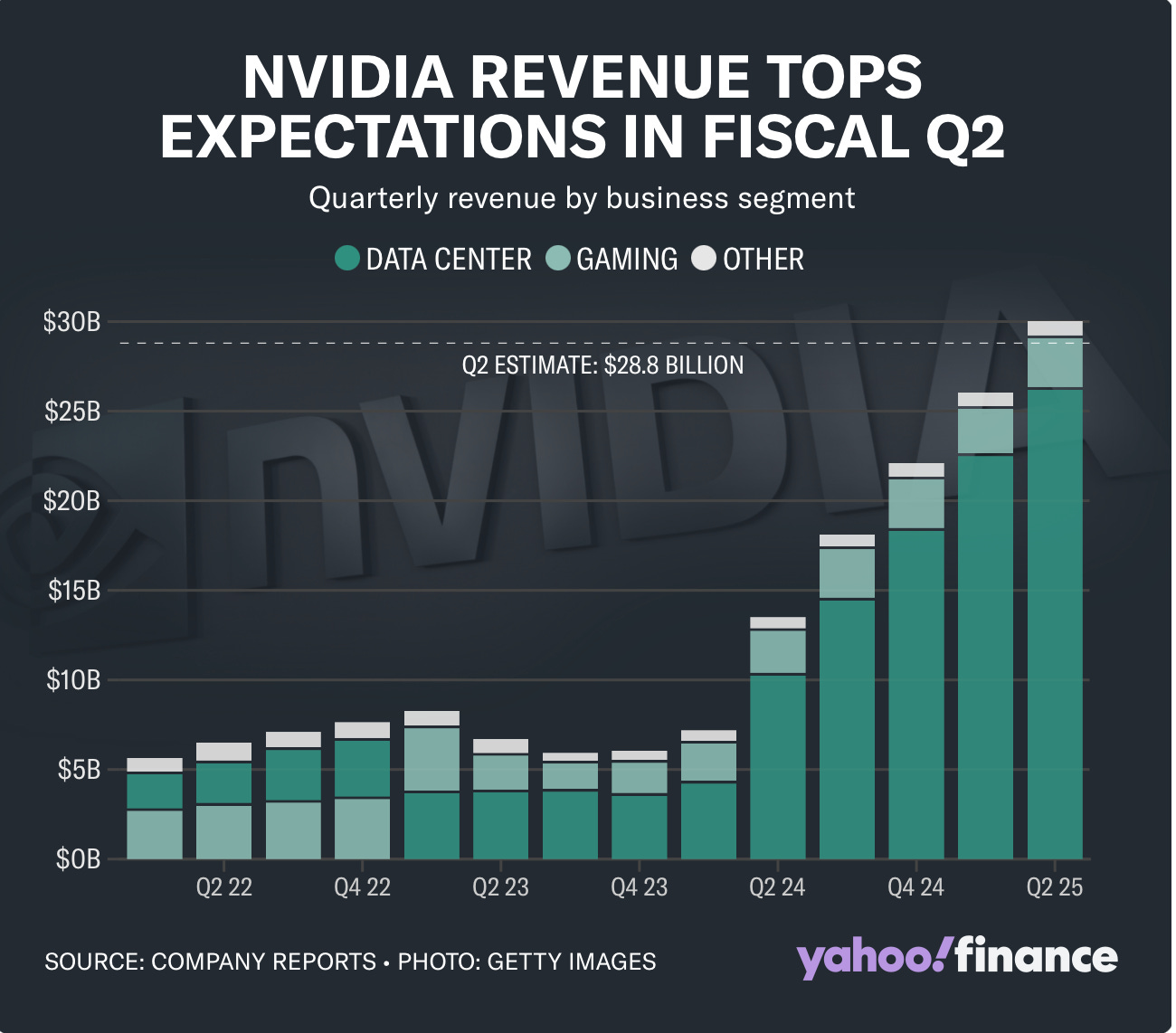

NVDA 0.00%↑ Q2 report was pretty impressive to me, but clearly not good enough for the rest of the market.

Here are the numbers:

Revenue - $30B vs $28.8B expected

EPS - 0.68 vs 0.64 expected

The company also announced a $50B share buyback program. Moreover, Nvidia guided revenue up for Q3 to $32.5B vs the expected $31.9B. For perspective, the company generated $30 billion dollars in one quarter. If you assume linear growth, that’s $10 billion per month and $2.5 billion per week.

There’s a lot of discourse going around whether or not the stock is insanely overvalued and if the company has any steam left. I think this is where it’s important to not just read the headlines and to not take them for granted.

Data center revenue came in at $26.3B vs $25B expected. Despite this being a 154% increase YoY, you have to realize that this growth is most certainly not sustainable in the long run. I’m not calling the top, but it’s definitely something to remember as time progresses because the company quite literally can’t keep growing at such astronomical pace forever.

Is that why Nvidia’s stock went down post earnings?

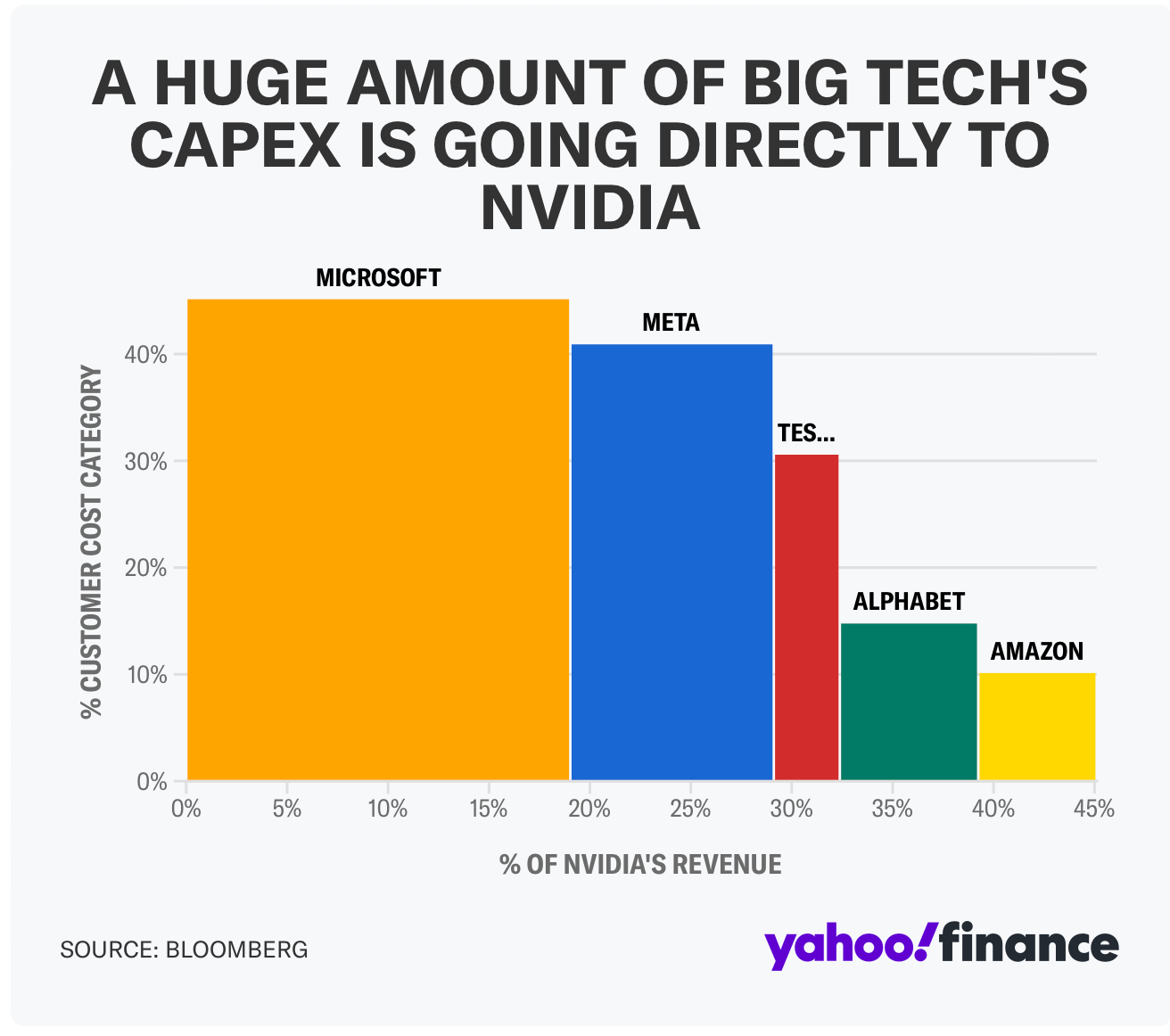

Funny enough, it would take an even crazier beat of expectations for Nvidia’s stock to react positively. Their stock is already up 150% YTD, a 6% pullback is minuscule in the grand scheme of things. I believe Nvidia’s growth is definitely not done in the near future, but maybe closer to to FY2025 and FY2026. Despite AMD 0.00%↑ playing catch up, it’s going to take a while before any company can even come close to competing with Nvidia. Almost half of Nvidia’s revenue is from your favorite tech stocks.

CEO Huang reminded investors that Nvidia chips aren’t used just for AI chatbots: entire infrastructures for search engines, robotics etc. are going to need chips that the company sells.

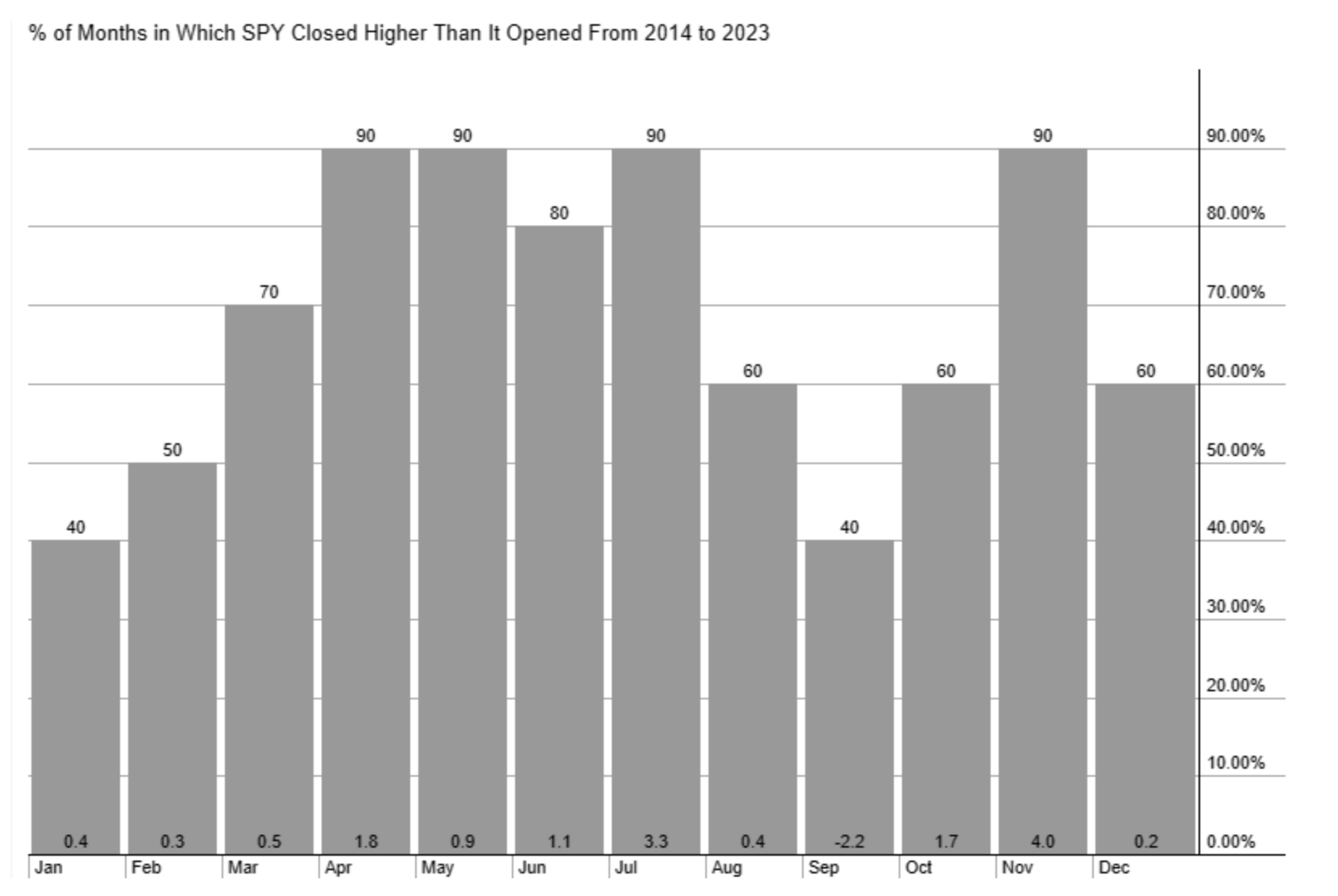

With the stock market not reacting as positively as some would have hoped to Nvidia’s earnings, it’s seeming to align a little too perfectly with seasonality. As August comes to a close, it’s to key to note that September and into October tend to yield negative returns for SPY 0.00%↑.

I’ve also mentioned in posts prior that we could potentially get a short term pull back from the rate cut in September. This might end up being a sell the news type of event. But of course, rate cuts in the long run are beneficial for the economy. Loans will be more accessible to businesses and people who are looking to purchase homes. I would be happy to be wrong, but very ready to BTD if we get that pullback.

Earnings Recaps

DG 0.00%↑ reported Q2 earnings and saw a 32% decline after guiding down.

Revenue - $10.21B vs $10.37B expected

EPS - $1.7 vs $1.79 expected

CEO Todd Vasos informed investors that low end consumers went for more consumable goods over home and apparel items, and seemingly more than Q1. Gross profit also decreased to 30% from 31% compared to previous year. Even though same store sales saw a surge, it was attributed to consumable items like food. This could be a potential red flag about the economy as a whole because over 60% of Dollar General’s customers are from households earnings less than $35,000 yearly. These consumers are now feeling even more financially squeezed.

LULU 0.00%↑ also lowered guidance but we’re seeing a boost to their stock price. Keep in mind, the stock is down almost 50% YTD.

Revenue - $2.37B vs $2.4B expected

EPS - $3.15 vs $2.93 expected

Lululemon from previous guidance expected annual growth to be around 12% but the company has now guided down to ~8% annual growth. Despite managing margins well with EPS coming in better than expected, the company saw same store sales increase only 2% versus the 6% anticipated.

The company had a botched leggings product line that was pulled within weeks from its launch. Yet, the company attributes to their lackluster performance to a reduction in styles, colors and prints. It’s also notable that the athleisure space has become extremely competitive but the company reaffirmed their confidence in bouncing back during the earnings call. With managing profitability well despite less revenue, I lean towards believing leadership at Lululemon.