From Bedside to Bottom Line: A Financial Check-Up of $HIMS

Is the healthcare industry being disrupted?

Welcome back to another edition of The Dividend Journal!

After a controversial Superbowl ad, HIMS 0.00%↑ reminds us about obesity epidemic in the US. The CDC in 2020 found that over 74% of adults in the US are overweight, with 43% of those obese. In more recent data, new CDC reports show that while obesity rates have not increased (first time ever in a decade), severe obesity is on the rise still.

The Superbowl ad continues to claim that the healthcare industry has the necessary drugs to combat this health issue but is being priced “for profits, not patients.” HIMS 0.00%↑ is the solution! With brand name Ozempic costing almost $1,000/month without insurance, HIMS offers a way more affordable alternative with their compounded GLP-1 medications offered at only $199/month.

With their stock rising over 200% in just four years since going public via SPAC, we have to take a deeper dive and see if they are actually changing the game.

In today’s post, we’re going to look at:

→ Understanding HIMS 0.00%↑ as a company

→ Analyzing their financial performance/projections

What does HIMS do?

HIMS’s mission statement is to “help the world feel great through the power of better health.” The company prides in being more than just a prescription writing entity. They are creating a personalized approach to healthcare on their technology platform. Basically, they’re a telehealth platform where patients can connect with real licensed healthcare providers who prescribe treatments. The intention is to disrupt the status quo and negative perspective of healthcare providers. It’s a common issue for people to feel a large disconnect and distrust with their healthcare providers, and the HIMS platform aims to bridge that gap. The prescriptions through HIMS are fulfilled through a network of partner pharmacies.

It’s interesting to note that the they recognize revenue as any online sales or consultation fees for products offered on their platform. They however do not disclose if any specific prescription is more significantly driving revenue. We can deduce not only for their Superbowl ad, but also through their purchase of a compounding factory in August of 2024 for weight-loss drugs, that a strong revenue driver is their Ozempic alternative.

Furthermore, HIMS stock also saw a 25% decline on February 21, 2024 after the FDA says Ozempic and Wegovy are no longer in short supply.

Are people adopting HIMS?

This is where it’s important to read between the lines. HIMS introduced their GLP-1 weight loss drug late May of 2024; a year over year comparison is going to produce some pretty funny numbers.

Here’s what I mean: total subscribers in Q3 grew 44% YoY. But, when you break it down quarter by quarter, total subscribers only increased by 9.6%. This is actually a decline from Q2 subscriber growth.

Another interesting shareholder letter presentation datapoint:

In Q3 of FY 2023, HIMS didn’t even offer GLP-1 injections. As a large driver of revenue, comparing the platform from before to after offering GLP-1 injections is not a really an apples to apples comparison.

I wholeheartedly believe that HIMS is definitely raising the bar for interactions between patients and healthcare providers. It’s definitely a step in the right direction for helping bridge the gap and instill more trust in our healthcare providers. This competition is good for the industry and will only benefit us as patients/consumers. As an investor, however, it’s important to know the whole truth for companies you are putting money into!

Financial Performance

The company is clearly very much in growth mindset, especially with the recent purchase of a US-based Peptide Facility. This will help the company optimize their supply chain in the U, which should help their margins in the long run.

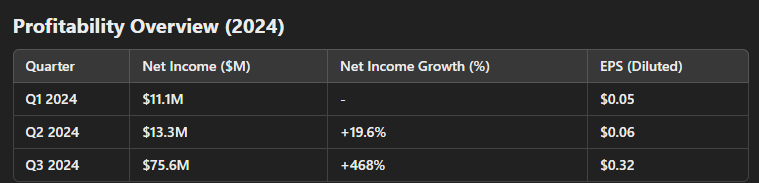

It’s undeniable that HIMS’s FY2024 performance show positives, with healthy revenue growth and increases in their profit margins.

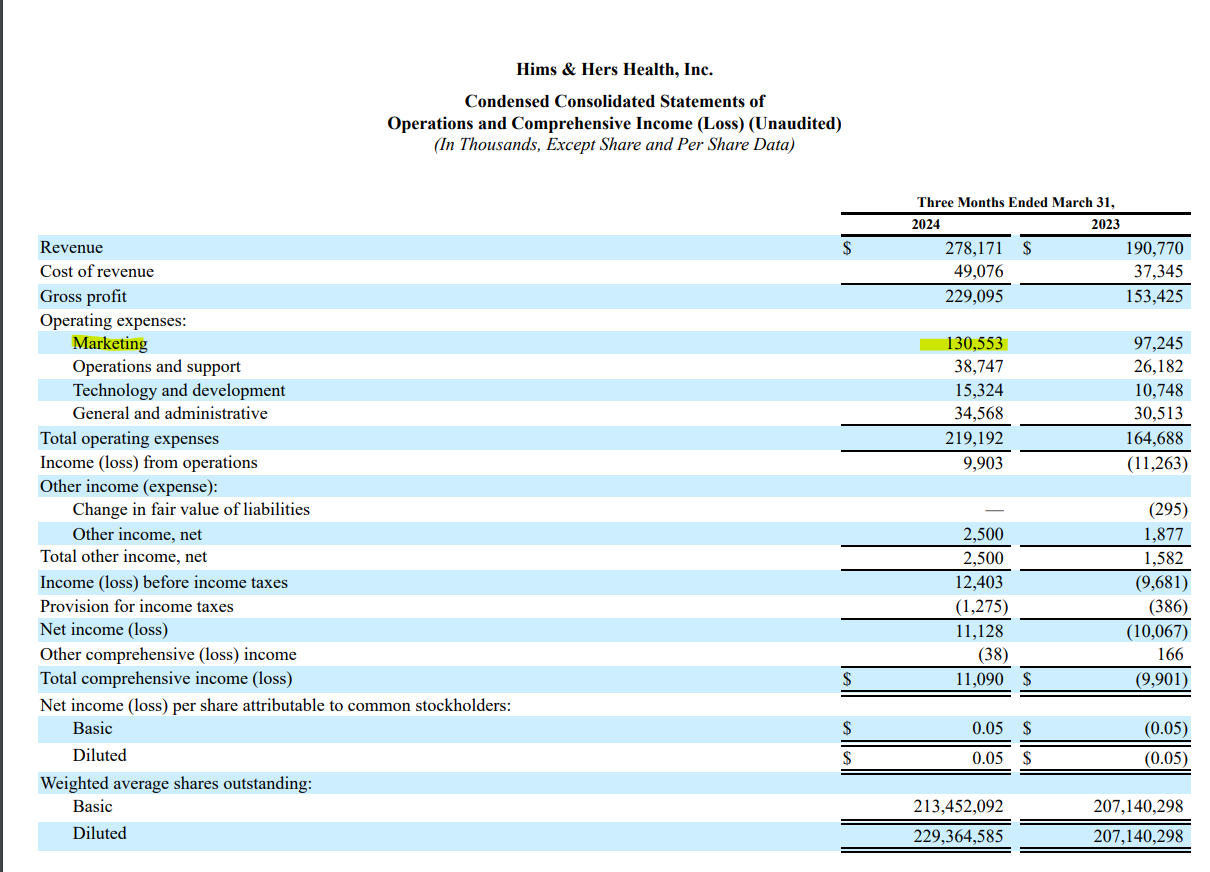

With a growing company that is trying to disrupt, this type of revenue growth is exactly what you want to see. A 27% increase in Q3 shows increasing interest and demand for HIMS products. While operating expenses outpaced the revenue growth, when you look at their income statement: the majority of that spend is on marketing.

This makes sense because the company needs to establish their brand name. The marketing also helps the company solidify their disrupting nature in the healthcare industry with their affordable prescription prices. Of course, this is something to closely monitor as the company continues to grow. Ideally, you would want to see marketing costs eventually decline as more consumers recognize the HIMS brand.

With the 27% increase in revenue in Q3, HIMS was also able to achieve a record net income of over $75M.

With no more Ozempic shortages, it’ll be interesting to see if HIMS is able to continue their revenue growth. A huge selling point for HIMS is still going to being a cheaper alternative to brand name Ozempic. I also think leaning into providing other prescriptions will also be easier to do with the acquisition of the California peptide facility.

Another key factor to continue observing is the consumer churn rate. In the Q3 FY2024 earnings call, HIMS reported that 70% of customers continued their GLP-1 subscription after 12 weeks of treatment. It’s important to note that the company does not really talk about the retention rate for their other products.

Investing in HIMS is definitely a risk on decision that carries some large risks. Will more consumers continue to adopt HIMS? Even so, personalized healthcare isn’t something HIMS can patent. Other telehealth companies/healthcare businesses can adopt their own versions and adapt to the competition.

Brand recognition can be very powerful, and if HIMS is able to establish themselves as the trustworthy brand to work with in healthcare, the future can be very bright. We’re seeing a clear pivot in their business and a higher focus on tackling weight loss in the US. Despite their controversial Superbowl ad, helping alleviate obesity in the US might be the path to success.