❄️Breaking the Ice: A Thorough Analysis of $SNOW

Organizations have only seemed to emphasize the need for data backing business decisions more as we progress into 2024. It’s become clear that the power of cloud computing is one of the keys to hitting profit margin goals and staying competitive. Snowflake Inc. ($SNOW), is a name that has become synonymous with innovation in cloud computing and data warehousing in this industry. But, has Snowflake’s growth dried up or will winter continue for this company?

In this article, we’re going to cover:

→ Snowflake Inc. company overview

→ $SNOW’s financial performance

→ The potential market opportunity and possible shortfalls

❄️Company Overview

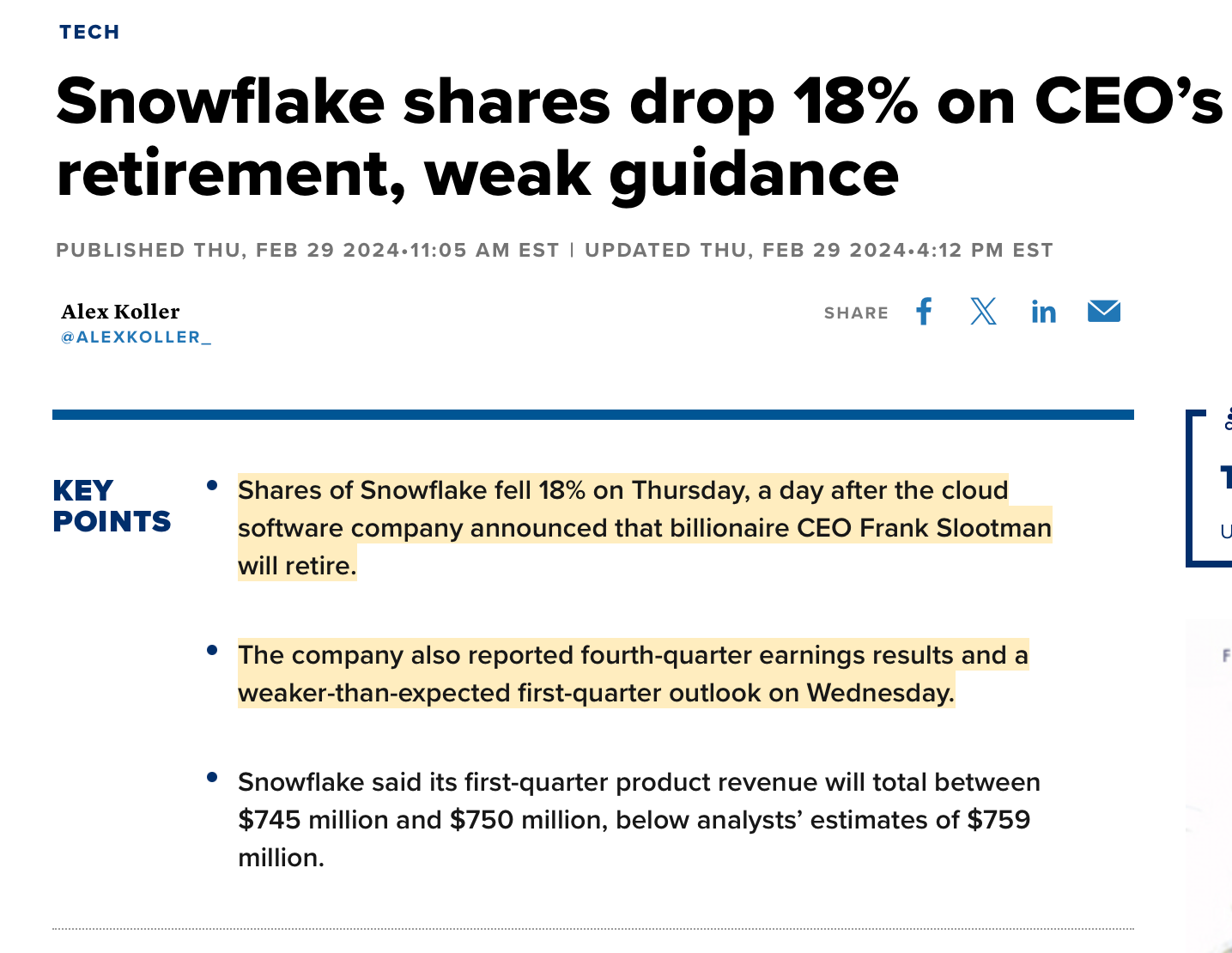

Snowflake Inc. was founded in 2012 and has quickly become a big player in the data warehousing industry. The cloud data warehouse company IPO’d in mid-September of 2020 and has seen pretty dramatic rises and slumps in its price since then. To close FY 2024, we saw a decline after their 4th quarter report—just after the CEO announced his departure.

Snowflake’s core product is their cloud-native data platform. This platform enables businesses to efficiently store, manage, and analyze vast amounts of structured and semi-structured data in real-time. Unlike traditional on-premises data warehouses, Snowflake's platform operates completely on the cloud. This platform also has an interesting structure where storage and computation is separated. Users can adjust computing resources without affecting storage data prices. This reduces the amount of downtime and maintenance required, and ultimately allows easier scalability.

❄️Financial Performance

Snowflake charges clients based on consumption: how much software is used. Users buy credits and then those are used as you consume them. This kind of reminds me of a similar model that companies like InKind use, where you buy credits on the app and consume them when you dine at restaurants.

This is different from traditional SaaS vendors who charge based on fixed monthly prices or annual subscription prices based on the number of users.

If market accelerates and economy improves, then consumption based SaaS Vendors like SNOW will perform better. Every incremental consumption leads to upside on numbers.

Downside is that when the economy weakens and is volatile, subscription based providers have predictable revenue growth and numbers.

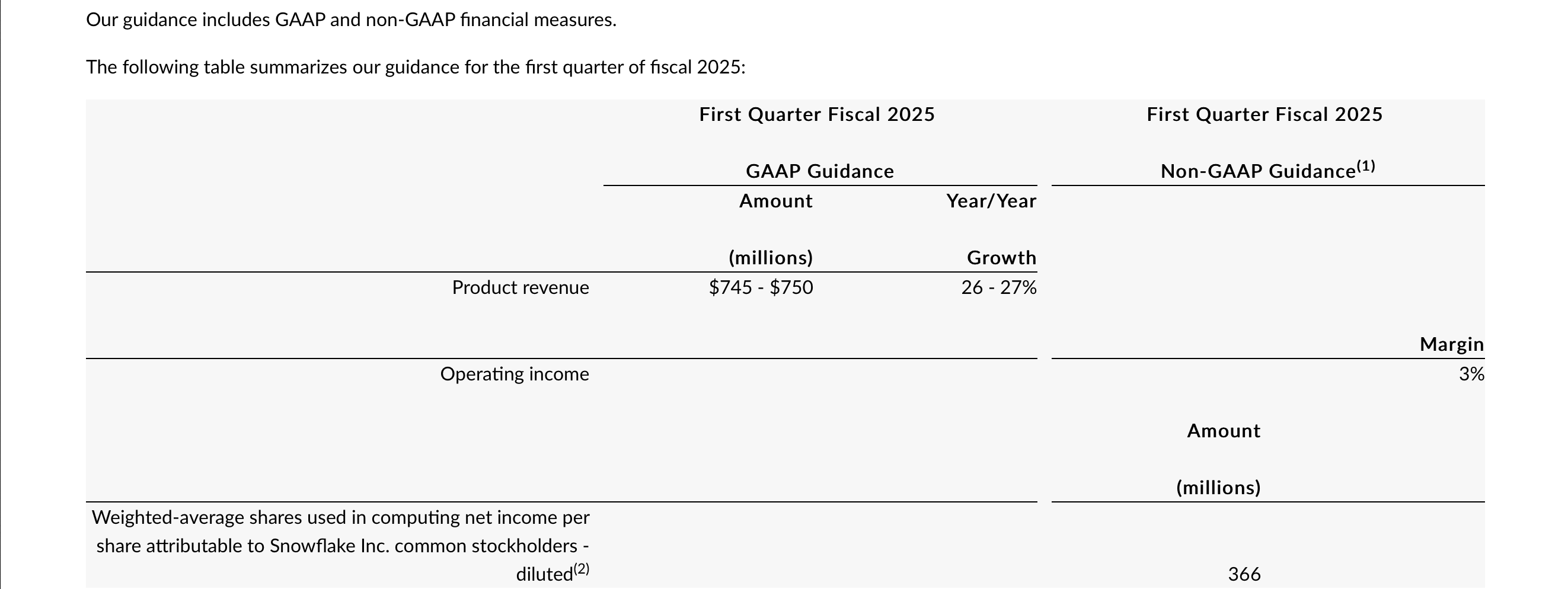

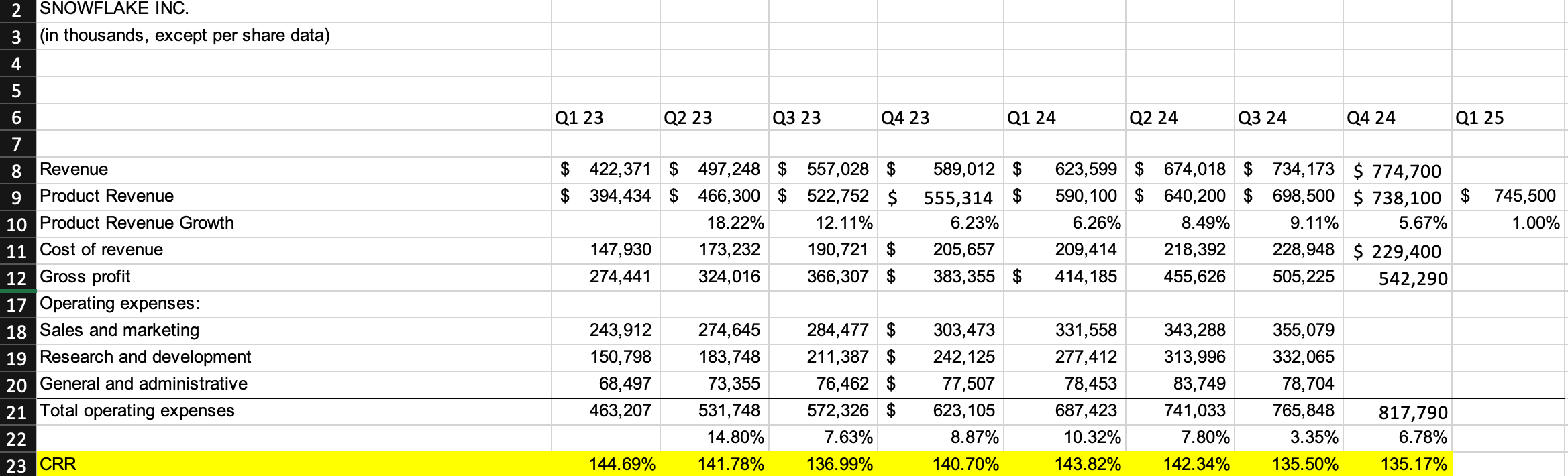

Snowflake in their earnings report project $745-750 million in product revenue in the first quarter of 2025. This guidance for the first quarter of FY25 is pretty lackluster. Do not be fooled by the 26-27% growth YOY. When you look at performance a quarterly basis, it’s actually only a 1% increase from Q4 of FY 2024.

The market also didn’t like this guidance as Snowflake’s stock price dropped 18% after their report went public.

Despite the projected slow down in revenue growth, there is positive news in the fact that their Cost to Revenue Ratio (CRR) is consistently decreasing.

CRR measures ALL operating expenses compared to the revenue that is being generated. If you only looked at revenue and cost of revenue, gross profit would be positive and you wouldn’t be looking at the entire picture. In reality, Snowflake is still operating at a loss because of their operating expenses. As a growing company, operating at a loss can be okay. Because Snowflake’s business model is more effected by the state of the economy, all eyes will be on how they manage their operating expenses relative to their product revenue generation in the next two fiscal years.

The CRR for Snowflake, as of Q4 of FY 2024, is interpreted as for every $1 in revenue, it costed $1.35. When compared on a quarter by quarter basis, Snowflake is lowering that cost of revenue. However, it’s obvious that it will take time before the company will be able to be operating in a profitable position. Investors will want to see Snowflake’s CRR continue to steadily decline. Eventually, Snowflake will reach an inflection point where they have optimized their business and will be able to operate profitably.

So, what’s the opportunity?

❄️Potential Long Opportunity

It’s clear that the previous CEO’s main objective was to go public and navigate the waters of appeasing stockholders while also balancing the values of the company. Now that that has been achieved, it makes sense the successor is Sridhar Ramaswamy, who has taken the helm of creating SNOW’s AI tools.

I believe the projected 1% growth in revenue is a conservative goal that Snowflake intends to easily hit. With the restructuring and shift in the company, I think it’s pretty smart to not set too high of an expectation. Underpromise and over deliver. Snowflake will still be spending lots on R&D and Sales & Marketing throughout the year as the generative AI craze continues. They will need to steadily spend to keep up with the competition. Logically, this implies that their revenue should see huge benefits. With Mr. Ramaswamy taking control of the company, Snowflake has an opportunity to be one of the market leaders in utilizing AI for data management.

Regardless of a long or short bias, Snowflake is an interesting stock to keep an eye on in 2024. Personally, I am slowly accruing Snowflake shares, with my first add to my portfolio at $165.30 on 3/13/2024.